|

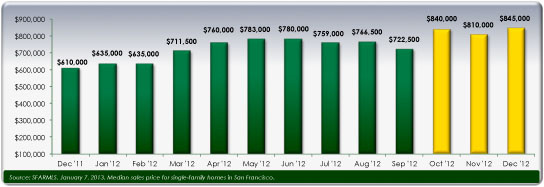

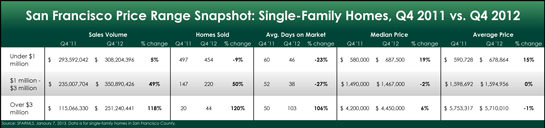

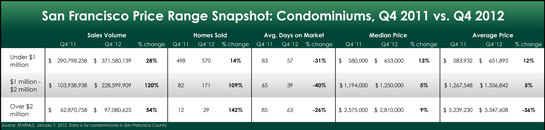

The year 2012 was one of the strongest in recent memory for real estate, and the frenzied pace continued through the fourth quarter, even accounting for a brief lull during the holidays. Pent-up buyer demand and an exceptionally tight supply of properties on the market meant that many homes sold quickly and with multiple offers. A balanced real estate market typically has a six-month supply of inventory, but the supply of single-family homes and condominiums in San Francisco hovered near record lows in the fourth quarter. Homes sold well across the city, and the condominium market, which had slowed in 2010 and 2011, came roaring back. San Francisco’s rebounding economy, particularly (but not exclusively) the growth in tech-sector jobs, brought many new buyers into the market, helping drive up home prices by double digits. Looking Forward: Job growth is a reliable indicator of real estate activity, and that factor alone promises a good year ahead for the San Francisco housing market. Interest rates are expected to remain near record lows through much of 2013, making the outlook even brighter. After a likely cyclical slowdown in January, we expect to see additional homes come on the market and sales take off in February and March. Median Sales Price The median sales price represents the midpoint in the range of all prices paid. It indicates that half the prices paid were higher than this number, and half were lower. It is not the same measure as “average” sales price. Single Family Home-Median Sales price

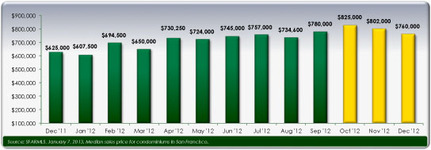

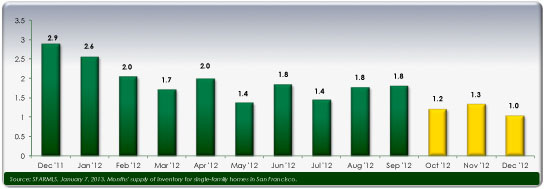

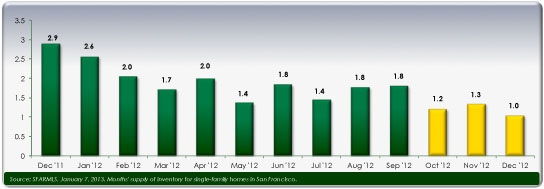

Condominiums-Median Sales Price Months’ Supply of Inventory The months’ supply of inventory is a measure of how quickly the current supply of homes would be sold at the current sales rate, assuming no more homes came on the market. In general, an MSI below 4 is considered a seller’s market; between 4 and 6 is a balanced market; and above 6 is a buyer’s market.

Single Family Homes – Months’ Supply of Inventory

Condominiums – Months’ Supply of Inventory

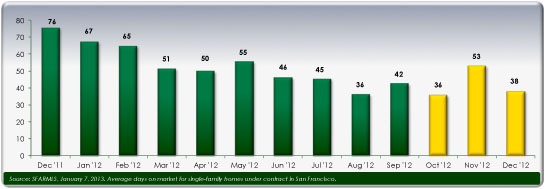

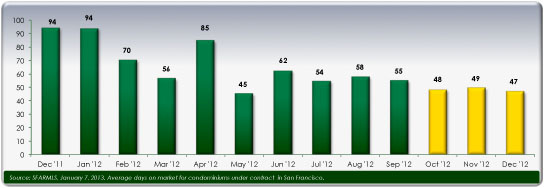

Average Days on the Market Average days on the market is a measure that indicates the pace of sales activity. It tracks, on average, the number of days a listing is active until it reaches close of escrow.

Single Family Homes – Average Days on the Market

Condominiums – Average Days on the Market

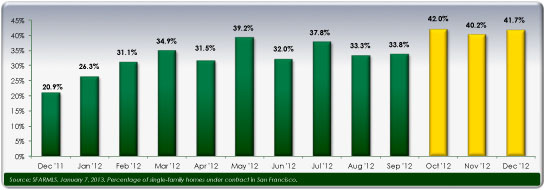

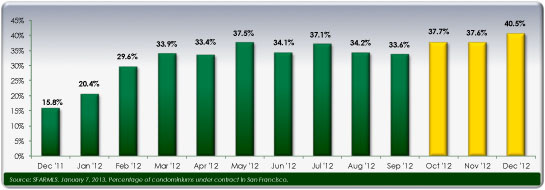

Percentage of Properties Under Contract Percentage of properties under contract is a forward-looking indicator of sales activity. It tracks expected home sales before the paperwork is completed and the sale actually closes.

Single Family Homes – Percentage of Properties Under Contract

Condominiums – Percentage of Properties Under Contract

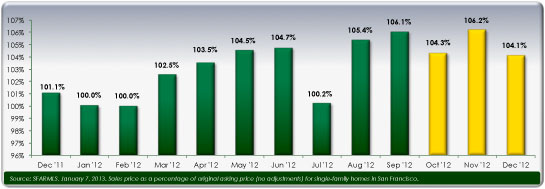

Sales Price as a Percentage of Original Price Measuring the final sales price as a percentage of the original list price, without price adjustments, determines the success of a seller in receiving the hoped-for sales amount, but it also indicates the level of sales activity in a region.

Single Family Homes – Sales Price as a Percentage of Original Price

Condominiums – Sales Price as a Percentage of Original Price

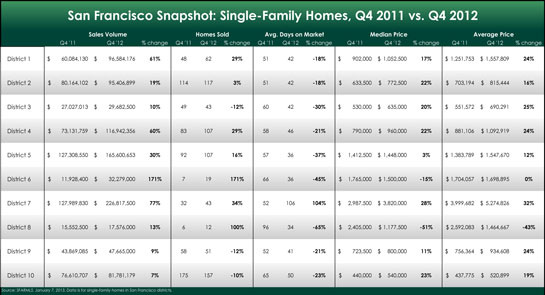

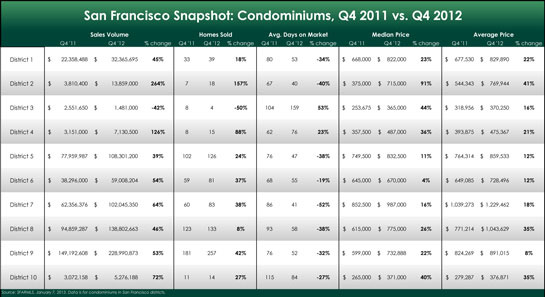

Delving Into San Francisco's Districts

San Francisco is defined by 10 separate districts, each of which encompasses several neighborhoods. District 1: Inner Richmond, Central Richmond, Outer Richmond, Jordan Park/Laurel Heights, Lake, Lone Mountain, Sea Cliff. District 2: Outer Sunset, Central Sunset, Inner Sunset, Outer Parkside, Parkside, Inner Parkside, Golden Gate Heights. District 3: Pine Lake Park, Merced Manor, Lake Shore, Lakeside, Stonestown, Merced Heights, Ingleside, Ingleside Heights, Oceanview. District 4: Balboa Terrace, Diamond Heights, Forest Hill, Forest Hill Extension, Forest Knolls, Ingleside Terrace, Midtown Terrace, Miraloma Park, Monterey Heights, Mount Davidson Manor, Sherwood Forest, St. Francis Wood, Sunnyside, West Portal, Westwood Highlands, Westwood Park. District 5: Buena Vista/Ashbury Heights, Clarendon Heights, Cole Valley/Parnassus Heights, Corona Heights, Duboce Triangle, Eureka Valley/Dolores Heights, Glen Park, Haight-Ashbury, Mission Dolores, Noe Valley, Twin Peaks. District 6: Alamo Square, Anza Vista, Hayes Valley, Lower Pacific Heights, North Panhandle, Western Addition. District 7: Cow Hollow, Marina, Pacific Heights, Presidio Heights. District 8: Downtown, Financial District/Barbary Coast, Nob Hill, North Beach, North Waterfront, Russian Hill, Telegraph Hill, Tenderloin, Van Ness/Civic Center. District 9: Bernal Heights, Central Waterfront/Dogpatch, Inner Mission, Mission Bay, Potrero Hill, South Beach, South of Market, Yerba Buena. District 10: Bayview, Bayview Heights, Candlestick Point, Crocker Amazon, Excelsior, Hunters Point, Little Hollywood, Outer Mission, Mission Terrace, Portola, Silver Terrace, Visitacion Valley.

2012 Set RecordsHere's to 2013! 2012 was a blistering year for San Francisco Bay Area residential real estate, as most of our regions tallied their highest number of home sales since 2005. Back in Q2 we said jobs would drive our housing markets, and we hit the nail on the head. Exceptional job growth in San Mateo, San Francisco, and Marin counties spurred home-buying demand at a pace not seen in other U.S. markets. Due to a limited inventory of homes for sale, we also got the most interesting dynamic of our record-setting year: the return of “bidding wars”, or multiple offers, in most markets at price points up to $1.5 million. In 2013 we predict more robust demand, as job growth expands into other Bay Area counties. Continuing constrained inventory will create price appreciation for the first time since 2007. And if the appreciation continues through summer '13, we will see “move-up buyers” re-enter the hunt for higher-end housing (over $1.5 million) in late August and early September. These buyers, who have been waiting patiently for their home values to rise so they can trade up to larger residences or better neighborhoods, will contribute to additional inventory in the mid-tier markets and improved demand in the higher end. Overall, we have a very positive outlook for Bay Area residential real estate in 2013. Whether you're looking to buy or sell, remember that real estate is hyperlocal — and your best ally is a real estate professional who can provide you with exceptional local insight, knowledge, advice, and decision support. Happy New Year! Luxury Home Buyers Changing Their Ways Goodbye, bling. Hello, quality and value.

That’s the new approach luxury home buyers are adopting in the San Francisco Bay Area, according to Alf Nucifora, chairman and founder of the Luxury Marketing Council of San Francisco. He says lessons learned from the recession, baby-boom buyers eyeing legacy purchases, and young tech turks who value function over form are fueling the trend. “The recession taught us that we can live without unnecessary extravagances,” says Nucifora. “And that has led to a systematic shift in the way people buy. We are less concerned with showing it on the outside but more concerned with enjoying it on the inside.” In addition, so-called baby boomers (born 1946 through 1964) now make up a significant portion of the luxury-buyer market, and they are shifting from making to preserving wealth. “We (boomers) played and we made and we splurged, but we don’t need the fancy cars, the watches, or the showplace home anymore,” he says. “Now it’s the notion of bespoke, of things crafted with an eye to enduring value. We have kids and grandkids and want a legacy to be handed off to them.” The young dot-com and IPO millionaires might not be thinking about their future family bequests, but many also eschew frippery for functionality. They choose jeans and T-shirts over Brioni suits and sink their money instead into elite experiences and artisanal comfort. They may not have the biggest house on the block, but there’s a La Cornue range in the kitchen and a custom Jacuzzi in the backyard. What this all translates to is a shift away from showy excess and toward a search for quality, value, and connoisseurship, especially in the $2 to $10 million range, says Nucifora. It’s the consumption of wealth on a quiet, introspective basis, as opposed to ostentatious display. “Buyers are now more focused on the view, the privacy, how good the kitchen really is -- things that go into the enjoyment of the family experience as opposed to letting me show my neighbors how big and wealthy I am,” he says. While luxury buyers still spend plenty of money, it’s now more often on things like interior remodels, home theaters, expensive custom cabinetry, or top-of-the-line appliances – items that create a high-end quality of life experience but are invisible to anyone on the outside. And even the most well-heeled buyers are looking for bargains. “They can easily afford to pay above listing price, but they want to get a deal because it affirms their sense of self, their smartness,” says Nucifora. What does this mean for 2013? Expect to see these trends continue, he says. Sellers in these price ranges would be smart to invest in staging, because today’s value-savvy luxury buyers are willing to shell out for the right experience – and a luxury residence with empty rooms or dated furnishings doesn’t fit that bill. “In buying real estate, it’s that visceral reaction when I walk in,” Nucifora says. And, he adds, bad presentation is obvious: “When you walk into some of them it’s like entering an abattoir.” Pie-in-the-sky pricing schemes will also be a thing of the past, even as home values rebound; buyers in the high-end market will continue to look for deals and choose substance over show-off style. The cachet of spending piles of money on a pile of bricks has worn somewhat thin, he says. “The recession taught us all that we can live without unnecessary extravagances, that we should look for quality, and really ask ourselves whether that purchase is absolutely necessary,” he says. “And most of us found out we can live without it.”

0 Comments

|

Alchemy Management Inc.Welcome to our Blog. Here we will post our latest projects, real estate news and successful marketing tools. Categories

All

Archives

February 2018

|

RSS Feed

RSS Feed